For decades, the narrative surrounding female entrepreneurship across Europe has been tethered to a patronising lexicon of “empowerment,” corporate social responsibility (CSR) photo opportunities, and modest micro-grants. While well-intentioned, these tokenistic frameworks did little to dismantle the structural capital starvation facing women-led Small and Medium Enterprises (SMEs). For the mid-market woman entrepreneur trying to scale a deep-tech firm in Munich, purchase a commercial pharmacy estate in Madrid, or digitise a manufacturing chain in Milan, the traditional high-street banking apparatus historically felt less like a launchpad and more like a brick wall.

However, as we progress through the mid-way point of 2026, a structural seismic shift is visible across the European financial architecture. Driven by rigorous regulatory frameworks, macroeconomic pressures, and an undeniable data pool proving the superior risk profiles of female borrowers, a new league of banking front-runners has emerged.

Supranational institutions and commercial banking giants are moving past superficial quotas. They are treating gender finance not as a niche moral imperative, but as a major untapped asset class. From the European Investment Bank’s (EIB) multi-billion euro institutional directives to localised commercial lending networks in Spain and Italy, the capital flows underpinning female economic inclusion have never been more targeted, quantifiable, or aggressive.

The €30 Billion Sovereign Blueprint: EIB and EBRD

To understand the scale of the transition, one must look at the apex of European financial policy. The European Investment Bank (EIB) Group has fundamentally altered the underwriting landscape by expanding its cumulative gender-focused financing architecture to well over €30 billion.

The institutional strategy shifted from passive advocacy to active market intervention. In March 2025, the EIB Group, in tandem with the European Commission, operationalised the InvestEU Gender Finance Lab. Rather than functioning as a standard grant fund, the Lab acts as an elite financial advisory hub and masterclass platform. Its explicit objective is to instruct European commercial banks on how to design, risk-model, and launch targeted, gender-responsive debt products. The financial logic is clear: by educating private lenders on how to leverage the structurally lower non-performing loan (NPL) ratios typically exhibited by women-led businesses, the EIB is systematically de-risking female commercial credit across the continent.

Concurrently, the European Investment Fund (EIF) has deployed the Empowering Equity Initiative. This targeted academy focuses on the supply side of private capital, engineered to improve gender equity across European venture capital and private credit markets.

In March 2026, the EIB Group formalised this systemic evolution by launching The EIB Group’s Gender Action Plan III (2026–2030). This policy ties structural funding allocation directly to gender-inclusive outcomes, requiring intermediary commercial banks to prove their capital is reaching female-led operations, with a particular focus on combining female business ownership with green climate resilience.

Further east, the European Bank for Reconstruction and Development (EBRD) continues to act as a crucial anchor for financial inclusion in developing markets and the Western Balkans. The EBRD’s signature Women in Business Programme long provided vital micro-loans and corporate governance mentorship.

However, its operations scaled dramatically through late 2025 and into 2026 via an expanded deployment alongside parallel EU EFSD+ guarantees and Western Balkans Investment Framework (WBIF) grants. By late December 2025, this partnership successfully mobilised strategic segments of its multi-million euro allocation pool to bridge critical funding deficits for micro-SMEs in Europe’s near-neighbourhood economies.

Furthermore, initiatives like the EBRD Women on Boards Regional Edition, launched in Bucharest, are intentionally preparing high-growth female startup founders to navigate the realities of institutional corporate governance.

By moving past superficial quotas and treating gender finance as a major untapped asset class, Europe’s banking front-runners are finally correcting legacy market inefficiencies.

Commercial Deployments: Ring-Fencing and Niche Capitalisation

While supranational mandates set the macroeconomic tone, the true test of financial inclusion occurs at the local commercial branch level. In this arena, the transition from rhetorical support to hard capital deployment is highly evident.

Mediobanca’s €200 Million Mandate (Italy)

In July 2025, Italy’s Mediobanca signed a benchmark agreement with the EIB to unlock a €200 million credit pipeline intermediated through its retail and consumer credit subsidiary, Compass Banca, aimed at supporting small businesses. This structure ensures the liquidity facility directly supports local families, micro-enterprises and female entrepreneurs.

By intentionally routing a substantial portion of these funds into the economically underserved industrial ecosystems of central and southern Italy, Mediobanca is actively countering geographical and gender bias simultaneously.

CBNK’s Precision Sectorisation (Spain)

Perhaps the most innovative, laser-focused deployment of the past year occurred via the EIB Group Forum in Luxembourg. In March 2025, the EIB extended a €150 million direct loan to Madrid-headquartered CBNK, the specialised commercial bank born from the strategic merger of Banco Caminos and Bancofar. Signed directly by EIB President Nadia Calviño and CBNK CEO Enrique Serra González, the launch of this specific pharmacy bond simultaneously served as the operational catalyst to open the broader InvestEU Gender Finance Lab advisory network across European commercial banking tiers.

This programme stands as the first intermediated financing framework in the European Union designed exclusively for women within a single professional sector. The capital is strictly designated to finance the creation, acquisition, or operational expansion of up to 600 women-led pharmacies and healthcare practices across Spain. By recognising that women represent the vast majority of qualified pharmacy professionals yet face disproportionate barriers when attempting to buy into equity ownership of those estates, CBNK has created a masterclass in sector-specific financial inclusion.

UniCredit’s Strategic Evolution (Pan-European)

Building on its historical foundations, such as its pioneering 2019 dual focus framework with the EIB, UniCredit has systematically integrated gender inclusion into its core commercial lending strategy through its latest milestone collaboration with the EIF. In January 2026, the institutions signed an expanded €445 million InvestEU guarantee agreement engineered to unlock up to €890 million in small business financing across Central and Eastern Europe.

This modernised facility pairs digital transformation and local climate objectives with InvestEU’s broader targeted social financing mechanisms. By routing resources through this programmatic architecture, the framework ensures that capital reaches underserved market segments, complementing UniCredit’s strategic focus on empowering female-led and youth-led small businesses within Europe’s green and digital transitions.

Financing women-led SMEs is not an exercise in corporate charity, it is a highly profitable commercial strategy that forward-thinking economists have backed for years.

BNP Paribas’ 6.2 Million Mass-Market KPI (Global)

For larger commercial banking conglomerates, financial inclusion is being evaluated on a massive scale, measured by the volume of previously unbanked or underbanked individuals brought into the formal financial ecosystem.

BNP Paribas has positioned itself as an industry leader by embedding explicit, audited human-centric targets directly into its corporate balance sheet. According to the group’s updated inclusion audit, BNP Paribas successfully extended specialised financial instruments, microfinance mechanisms, and targeted SME accounts to 5.5 million underserved individuals globally over the course of 2025.

Rather than pausing to celebrate, the institution is aggressively tracking toward an audited target of 6.2 million beneficiaries by the close of 2026. This mass-market inclusion is largely powered by its high-performance digital banking vehicle, Nickel, alongside deep-tier microfinance institution partnerships across Western Europe.

Simultaneously, the BNP Paribas Foundation has expanded its focus past simple corporate philanthropy. In early 2026, the foundation deployed a coordinated, cross-border operational network spanning five key European operating bases: Germany, Luxembourg, the Netherlands, Poland, and Portugal. This programme bypasses traditional retail banking limitations by funding grassroots female entrepreneur networks, offering early-stage business owners the foundational accounting, legal, and operational infrastructure required to become eligible for institutional bank loans later in their corporate lifecycles.

![]()

Non-Bank Disruptors and the Alternative Capital Landscape

While traditional commercial banks are modernising their lending strategies, they remain fundamentally ill-equipped to finance the bleeding edge of innovation. Traditional debt financing mandates predictable cash flows or physical collateral, which are assets that deep-tech, biotechnology, and advanced engineering startups simply do not possess during their multi-year R&D cycles. This structural market failure creates a financing chasm that is increasingly being filled by non-bank disruptors and highly structured, non-dilutive sovereign capital mechanisms.

The urgency for these alternative capital instruments is underscored by severe systemic imbalances within European venture capital. Recent data reveals that all-female founding teams capture a microscopic 3% of overall startup capital across the continent. Even when looking at broader gender-diverse teams in high-stakes fields like deep-tech, female-led ventures secure just 11.4% to 14% of sector funding, a figure that has remained virtually stagnant for nearly a decade. For female entrepreneurs operating in these high-failure-rate, capital-intensive realms, the lack of asset-backed collateral combined with implicit investor bias creates an almost insurmountable barrier to entry.

In this heavily restricted financing landscape, the European Union’s institutional Women TechEU initiative, originally managed directly by the European Innovation Council and SMEs Executive Agency (EISMEA), has established itself as an essential alternative funding driver. The programme is currently executing a coordinated rollout of €12 million in equity-free capital, strategically structured to bypass the collateral bottleneck entirely. Rather than forcing founders to surrender vital equity early in their funding cycles to predatory pre-seed investors, the initiative injects a flat €75,000 grant directly into each selected company.

This current funding cycle is engineered to scale 160 high-potential, women-led companies, providing them with the financial runway required to build minimum viable products (MVPs) and clear initial regulatory hurdles. Crucially, the programme recognises that capital alone cannot bridge the gender gap. The financial injection is paired with premium Business Acceleration Services (BAS), which grant founders elite access to bespoke business development tracks, intensive executive coaching, and direct, curated introductions to premium venture capital networks.

For the investment community tracking this pipeline, the open call for the current cohort features a strict proposal submission deadline on 30 June 2026 at 17:00 CEST. By de-risking these ventures at the ultra-early stage, this sovereign mechanism effectively transforms un-bankable research into highly attractive targets for subsequent private equity and larger EU scale-up funding.

Opinion: Moving Past Tokenism to Real Economic Equity

The data collected across Europe over the past 12 to 18 months proves a fundamental truth that forward-thinking economists have stated for years: financing women-led SMEs is not an exercise in corporate charity; it is a highly profitable commercial strategy.

Historically, the banking sector approached female entrepreneurs with risk models loaded with systemic bias. Women were frequently viewed as higher-risk or lower-scale, despite consistent empirical data showing that female-led businesses generate higher revenue per euro of invested capital and maintain lower default rates on commercial debt than their male counterparts. By ring-fencing capital, creating sector-specific loan facilities like CBNK’s pharmacy initiative, and establishing dedicated advisory hubs like the InvestEU Gender Finance Lab, Europe’s banking front-runners are finally correcting these outdated market inefficiencies.

However, significant challenges remain. While supranational capital from institutions like the EIB and EBRD is abundant, the mid-tier commercial banking sector across parts of Eastern and Southern Europe remains conservative. Too many local lenders still rely on legacy underwriting procedures that penalise non-traditional career paths or businesses without significant real estate collateral.

To truly capitalise on this momentum as we look past 2026, the European banking industry must see a more widespread adoption of the data-driven risk modelling championed by the InvestEU Gender Finance Lab. Commercial banks must completely decouple their underwriting from gendered assumptions and fully embrace algorithmic, performance-based credit evaluations.

Europe’s economic future depends heavily on its ability to innovate and compete globally. At a time when the continent is navigating complex supply chain reconfigurations and a massive green energy transition, locking out half of the entrepreneurial talent pool through outdated lending biases is an economic luxury Europe simply cannot afford.

The banking front-runners of 2026 have proven that when you provide female entrepreneurs with real, institutional capital rather than mere rhetorical support, they do not just build businesses—they rebuild entire market ecosystems. The blueprint has been drawn; it is now up to the remainder of the European financial sector to follow suit and fund the future.

When you provide female entrepreneurs with real institutional capital rather than mere rhetorical support, they do not just build businesses, they rebuild entire market ecosystems.

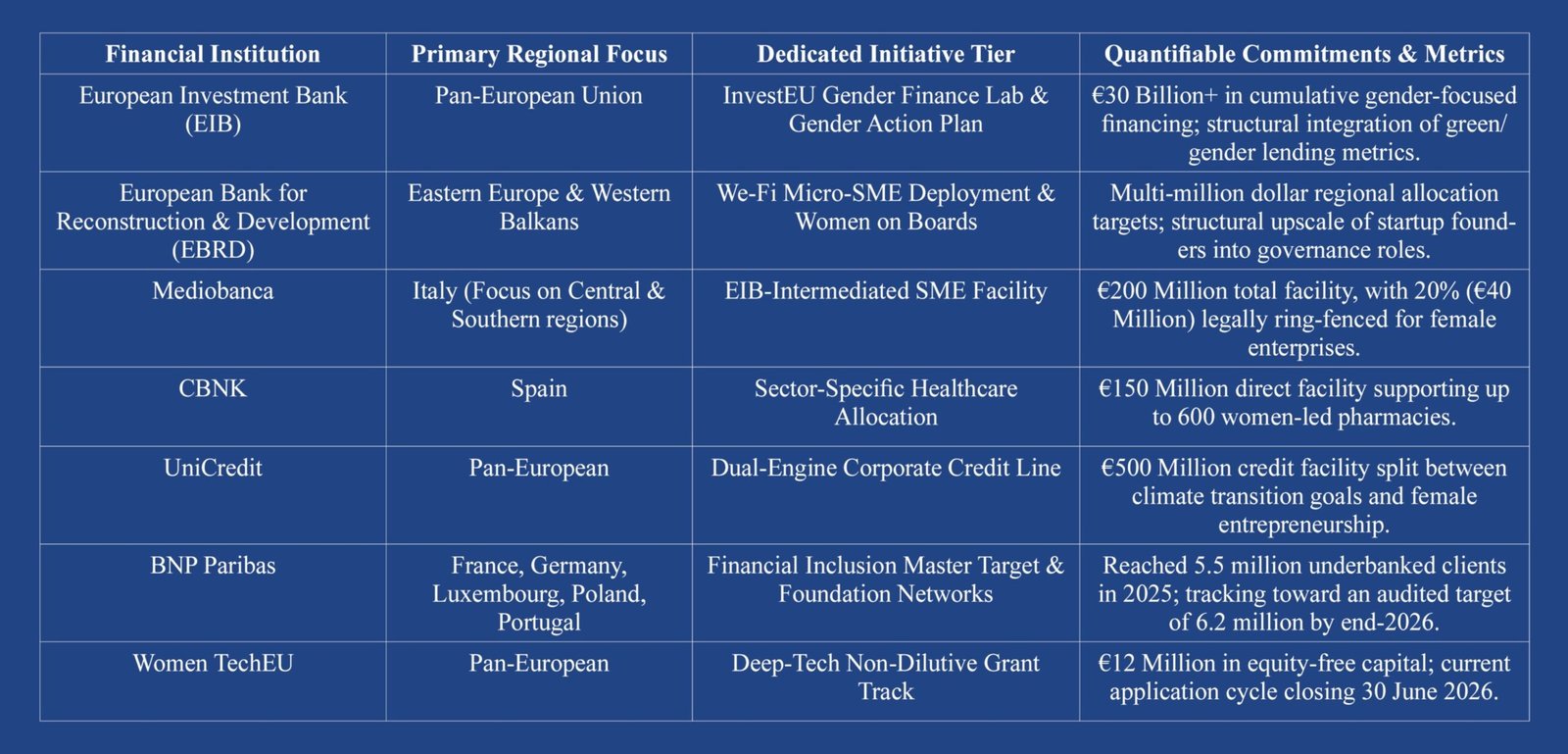

Summary of Key Institutional Initiatives (2025–2026)

To provide a concise reference for industry observers, the table below summarises the principal institutional initiatives currently active across Europe.