For most of the last decade, the question asked of women managing work alongside caregiving was framed as a personal one: how do you cope? It was a question that absolved employers of any responsibility and placed the entire burden of an ageing parent, a young child or a health condition squarely on the woman trying to hold it all together. The boardroom stayed separate from the living room, and the gap between them was treated as a private logistics problem, not a corporate one.

That framing has been broken open, not primarily by legislation, but by a generation of founders who reached their own breaking point and decided to build what was missing. Kate Ryder watched friends suffer through pregnancy with no clinical support and virtually no access to specialists. In 2014, she founded Maven Clinic, which has since grown into the largest virtual clinic for women’s and family health, valued at $1.7 billion and working with more than 2,000 employers worldwide. Her story is not unusual in this sector. It is the template. These founders stopped asking how individuals could cope and started asking how infrastructure could scale. The result is a new class of technology company: the care-tech unicorn, worth a billion dollars or more, built on the straightforward argument that care is not a personal inconvenience but a structural economic problem with a commercial solution.

Care is the work that makes all other work possible.

The Size of the Problem

Before looking at the companies, the scale of what they are addressing needs to be clear.

According to the International Labour Organization (ILO), 708 million women worldwide are currently outside the labour force because of unpaid care responsibilities. That figure comes from data across 125 countries and was published in October 2024. Among women aged 25 to 54, two-thirds of those outside the workforce cite care as the primary reason. By contrast, only 40 million men are out of the workforce for the same reason.

In the United Kingdom specifically, the cost is measurable. An NHS Confederation report found that inadequate workplace support for menopause alone costs the UK economy around £1.5 billion each year, largely because experienced women leave employment before they need to.Parliamentary data highlights that approximately one million women in the UK have left the workforce due to menopausal symptoms, while research from the CIPD found that 67% of women aged 40 to 60 surveyed reported those symptoms had a negative impact on their performance at work.

These are not fringe statistics. They represent a structural drain on talent pipelines and a measurable financial loss for businesses that have not invested in care infrastructure. The founders building care-tech companies are, in effect, offering employers a way to stop that drain.

What the Market Looks Like in 2026

The femtech and care-tech sector has moved well past the stage where it needed to prove itself to investors. The two terms are often used interchangeably, but they cover distinct ground: femtech focuses on women’s biological health, from fertility to menopause, while care-tech addresses the structural and logistical side of care delivery, including eldercare navigation, family benefits platforms and AI-assisted clinical operations. In 2026, the two are converging, with the most competitive companies now operating across both dimensions. The global femtech market was valued at approximately $60 to $73 billion in 2025, depending on which analyst you consult, and multiple forecasts project it to reach between $140 billion and $297 billion by 2035. Even the most conservative projections point to a compound annual growth rate of around 9% through the next decade.

Venture capital has responded accordingly. Funding for women’s health startups grew by 55% in 2024, reaching a total capital pool of approximately $2.6 to $3 billion for the year. The first quarter of 2026 accelerated this trend further: US digital health funding totalled $4 billion across 110 deals, exceeding the same period in 2025 by $1 billion, with the average deal size reaching its highest point since the fourth quarter of 2021.

What has changed is not just the volume of capital but the quality of the conviction behind it. Investors who were cautious about women’s health ten years ago are now writing nine-figure cheques with confidence, because the performance data from the past two to three years has removed the guesswork.

The Unicorns: Who They Are and What They Built

Flo Health is perhaps the clearest example of how this market has matured. The London-based women’s health platform, founded in 2015 and backed by a team of more than 120 doctors and health experts, became the first purely digital consumer women’s health app to achieve unicorn status when it raised more than $200 million in a Series C investment from General Atlantic in July 2024. That round pushed Flo’s valuation beyond $1 billion. At the time of the raise, the app had nearly 70 million monthly active users and close to 5 million paid subscribers. Gross bookings for 2024 were projected to exceed $200 million, representing roughly 50% year-on-year growth. Flo also became the first European femtech company to reach unicorn status, a milestone that shifted the conversation about where care-tech innovation could happen.

Flo’s proposition is straightforward: give women a single platform to track and understand their health across menstruation, conception, pregnancy and menopause. But the commercial logic behind it is more interesting. Women are the primary healthcare decision-makers in most households. Building trust with them at scale, through data and clinical credibility, creates a defensible position that a generic health app cannot replicate.

Midi Health reached unicorn status in February 2026, when it closed a $100 million Series D round led by Goodwater Capital, with participation from Google Ventures, Foresite Capital and Serena Ventures. The round brought Midi’s total funding to $250 million since it was founded in 2021 and valued the company at over $1 billion.

Midi was built around a specific and previously underserved gap: perimenopause and menopause care. Two million American women enter menopause each year. A Mayo Clinic study estimated that untreated menopausal symptoms cost the US economy over $26 billion annually in medical expenses and lost productivity. Midi’s founder and CEO, Joanna Strober, recognised that this was not a wellness problem but a clinical and economic one. The company built an insurance-covered, AI-enabled telehealth platform that now serves more than 25,000 patients per week across all 50 US states, with a clinician network of 500 providers. Its AI engine handles chart analysis, scheduling, triage and documentation, freeing clinicians to focus on the work that requires human judgement.

Midi is now expanding beyond menopause into what it calls lifelong care, covering cardiology, obesity management, autoimmune survivorship and longevity. The pivot reflects a broader pattern in care-tech: companies that start by solving one underfunded problem in women’s health discover that the market for the next problem is equally large.

Talkiatry, the US-based virtual psychiatry provider, closed a $210 million Series D in February 2026, led by Perceptive Advisors with participation from Andreessen Horowitz, Sofina and Left Lane Capital. The round brought its total funding to more than $400 million. Talkiatry employs more than 800 full-time psychiatrists and 300 therapists, operates across 45 states, and has delivered 3 million patient visits to date. It is in-network with more than 100 insurers covering over 170 million lives.

The mental health angle is directly relevant to care-tech’s broader thesis. Women are disproportionately affected by anxiety, depression and burnout, conditions that worsen when care responsibilities go unsupported. Employers are increasingly purchasing access to platforms like Talkiatry specifically to address caregiver burnout, which sits alongside physical health and eldercare navigation as one of the leading drivers of early exit among senior women. A platform that removes the friction from accessing psychiatric care, through insurance coverage, technology-assisted matching and employed clinicians rather than contractors, addresses a gap that employers increasingly recognise as a retention and productivity issue, not just a personal health matter.

The Business Logic: Why Employers Are Paying Attention

What connects Flo, Midi and Talkiatry is not just their valuations. It is where they sit in the supply chain. All three sell, at least in part, to employers and insurers rather than purely to individual consumers. This B2B2C model is the financial engine of the care-tech sector.

When an employer pays for a subscription to give its workforce access to a menopause telehealth platform, or a mental health provider, or a fertility benefit, it is making a retention calculation. The cost of losing a senior employee, recruiting a replacement and waiting for them to reach the same level of output is significant. Research from professional services and legal sectors consistently shows that the exit of a partner-level employee costs multiples of their annual salary.

The Employment Rights Act 2025 in the UK has added a compliance dimension to this calculation. From April 2026, large employers with 250 or more employees are encouraged to publish menopause and gender pay gap action plans. By 2027, these requirements are expected to become mandatory. Employers who have already partnered with care-tech platforms are better positioned to meet this standard than those who have not.

A broader indicator of corporate adoption comes from employee benefits data. In 2026, organisations in the US can draw on an increased dependent care flexible spending account limit of $7,500 per household. It is employer contributions to these accounts, rather than the limit itself, that determine how meaningfully care-tech platforms become accessible to employees in practice. Major employers are expanding childcare, eldercare and family leave benefits as a direct response to retention pressures in competitive talent markets, and the FSA mechanism gives them a tax-efficient route to fund that expansion.

The Funding Picture: Who Is Backing This and Why

The institutional shift in how venture capital treats women’s health is real, but the data reveals a paradox at the heart of the market.

In 2025, female-founded companies raised a record $73.6 billion, capturing approximately 25 per cent of total US venture deal value. However, this figure is heavily skewed by two massive AI deals: Anthropic (co-founded by Daniela Amodei) and Scale AI (co-founded by Lucy Guo) accounted for roughly 40% of that entire sum. When examining all-female founding teams specifically, the picture is starker: these companies received roughly 2% of all venture capital globally. The disparity is even more pronounced in femtech specifically: companies with all-female founding teams received 0.6% of femtech VC funding in 2025, whilst companies with both male and female co-founders captured 45% of that capital.

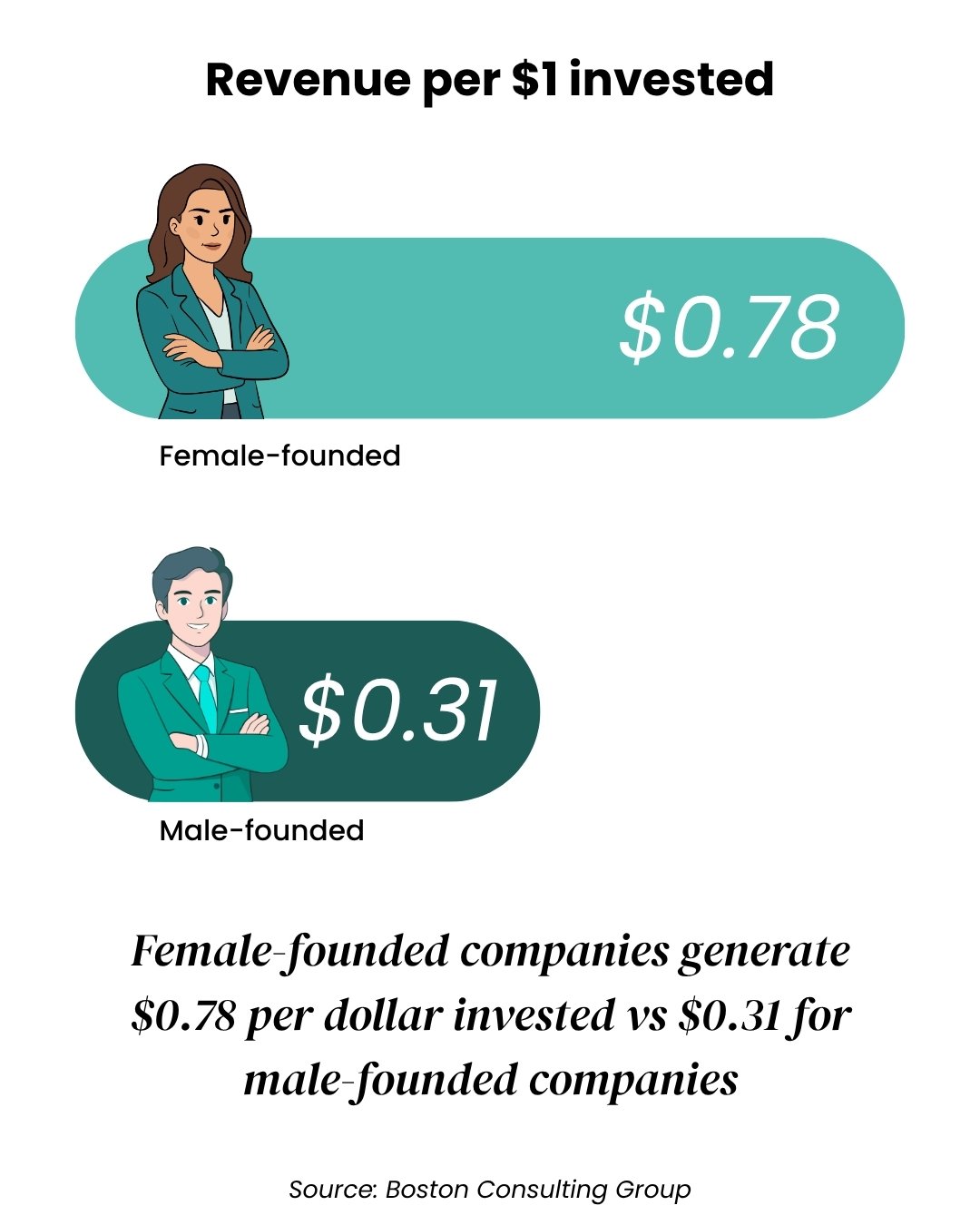

The reason institutional investors are increasingly backing companies like Flo, Midi and Talkiatry is not sentiment. It is performance. According to landmark Boston Consulting Group research, women-founded companies generate 78 cents of revenue for every dollar of funding invested, compared to 31 cents for male-founded companies. This efficiency gap is structural, not accidental. When founders operate with constrained capital, every deployment becomes critical. Profitability is not a distant concept. It is survival.

The care-tech sector has benefited from this dynamic. Femtech companies reached a combined valuation of $28 billion in 2024. Funding for the sector exceeded $1.1 billion globally in 2024, representing a resilient slice of digital health investment, though this marked a structural shift from the hyper-inflated venture peaks of 2020. What has changed is not the overall funding level but the quality of conviction behind it. The performance of companies like Flo (70 million monthly active users, 50% year-on-year growth) and Midi (25,000 patients per week) has shifted the conversation from whether care-tech is viable to which companies will capture the largest share of a structural market.

A select group of European female-founded companies achieved unicorn status by 2025, contributing to a growing but exclusive club of diverse-led tech giants across the continent. The Q1 2026 digital health data reinforces the shift toward scale: the period saw a distinct concentration of large, $100 million-plus cheques funnelled into companies with contracted revenue, clinical evidence and deep system integration. The message from institutional capital is unambiguous. It is no longer interested in pilots. It wants companies that have already proven they can operate at scale.

The Longevity Context

Running behind all of this is a demographic shift that makes the care-tech opportunity structural rather than cyclical.

The global longevity economy is projected to reach $27 trillion by 2026 to 2030, depending on the forecast used. By 2030, one in six people globally will be over 60. In the US, the over-65 population will outnumber under-18s for the first time by 2034. In the UK and across Europe, the workforce is ageing and shrinking simultaneously, placing greater pressure on the women who are most likely to be managing care for both older relatives and children at the same time.

The US Census Bureau estimates there will be 73 million baby boomers, all aged 65 or older, by 2030. That cohort will require care, and the majority of that care will fall on family members, most of them women, unless scalable alternatives exist. Care-tech companies are building those alternatives. Not as a charity or a social enterprise, but as commercially viable businesses with repeatable revenue models, because the demand does not diminish and cannot be outsourced abroad or automated away entirely.

What This Means for Employers and Employees

The practical implication of the care-tech sector’s growth is that the list of what constitutes a competitive employment offer is changing.

Salary, title and flexible working are now table stakes in most professional sectors. What differentiates employers in 2026 is the quality of their care infrastructure: access to menopause support, mental health provision, eldercare navigation, fertility benefits and neurodiversity support. These are not perks. They are retention tools, and they are becoming compliance requirements.

For women in the workforce, particularly those in the 40 to 60 age bracket who are most likely to be managing simultaneous care responsibilities for children and ageing parents, the availability of employer-backed care-tech platforms has a direct effect on whether they can remain in senior roles. The data from the NHS Confederation and from Hertility points to a group that is leaving the workforce not because it wants to, but because the infrastructure to stay does not exist. Care-tech companies are building that infrastructure. The employers who adopt it first will have a competitive advantage in attracting and retaining the experienced talent that their competitors are losing.

The Road Ahead

The care-tech sector in 2026 is not at the beginning of its growth curve, but it is not at the end either. The unicorn status achieved by Flo, Midi and others validates the market, but the proportion of employers who have moved from awareness to active adoption remains limited. The UK regulatory push around menopause action plans will accelerate this. So will the growing body of evidence linking care benefits to measurable retention outcomes.

The founders driving this sector built companies out of necessity. They identified problems that had been treated as personal and private, reframed them as structural and economic, and found investors willing to back the thesis. The capital is now following the data. And the companies that will define the next decade of work are not being built around perks or goodwill. They are being built around the things that people, and the businesses that employ them, simply cannot function without.